It’s Not You, It’s 23andMe

An Object Lesson in Strategic Overreach

In the early 2000s, amid the buzz of consumer empowerment and Web 2.0 optimism, 23andMe launched with a radical proposition: that individuals could, and should, access and interpret their own genetic data. For a brief moment, the company stood at the confluence of novelty and legitimacy—a pioneer making personal genomics not only accessible but emotionally resonant.

By 2024, however, the narrative had shifted. A SPAC-fueled public listing, failed vertical integration, and eroding consumer trust had transformed 23andMe into something of a cautionary tale—an archetype of what happens when a company with a singular strength mistakes optionality for inevitability.

This is the story of how a $99 ancestry gift kit grew up, tried to become a healthcare empire, and discovered the hard way that strategic coherence still matters.

From Gift Shop to Genomics

Founded in 2006, 23andMe’s initial value proposition was compelling and clear: it provided an affordable and user-friendly entry point into the once esoteric world of DNA testing. With strong early backing from Google, the company scaled rapidly, driven by a powerful combination of seasonal gifting, viral storytelling, and direct-to-consumer branding.

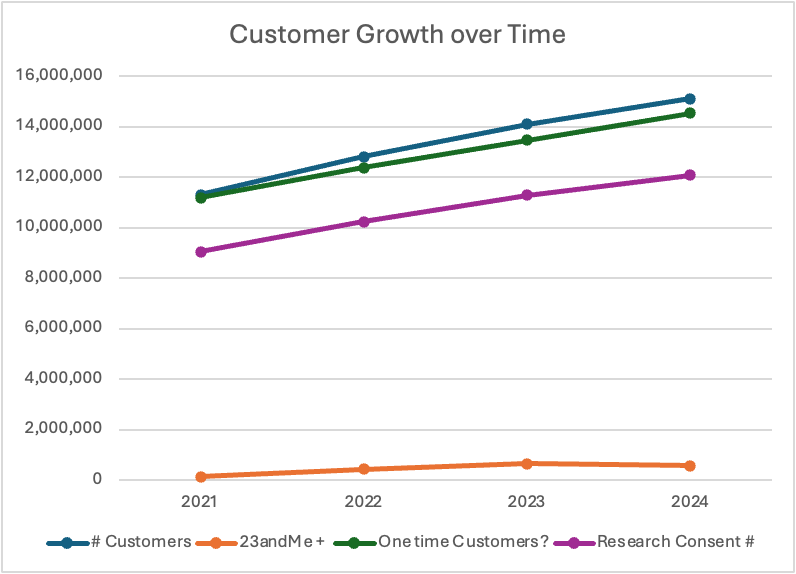

By 2021, it had boasted over 11 million customers. As of 2024, that number exceeded 15 million—with 80% of customers consenting to research use—giving the company one of the world’s largest genotype-phenotype databases. At the time, 23andMe had done what few others had: turned consumer curiosity into a data asset of staggering value.

But consumer curiosity is not consumer commitment. The majority of 23andMe’s customers were one-time buyers, driven by novelty rather than long-term utility. This fundamental dynamic—the tension between strategic ambition and consumer perception—would ultimately define the company’s missteps.

The Pivot to Health: Strategic Logic, Operational Chaos

In 2018, 23andMe partnered with GlaxoSmithKline (GSK), marking a definitive pivot from consumer DNA kits to B2B data monetization in pharmaceutical R&D. By 2020, the company had also launched 23andMe+, a subscription platform offering expanded health insights. In 2021, it acquired Lemonaid Health for $425 million, signaling a move into telemedicine and vertically integrated care.

The intent was clear: 23andMe aspired to become a full-stack precision health platform, combining diagnostics, insights, and interventions. On paper, this strategy satisfied multiple corporate strategy tests—complementarity, potential synergies, and access to an attractive, high-growth market.

In practice, it failed on execution.

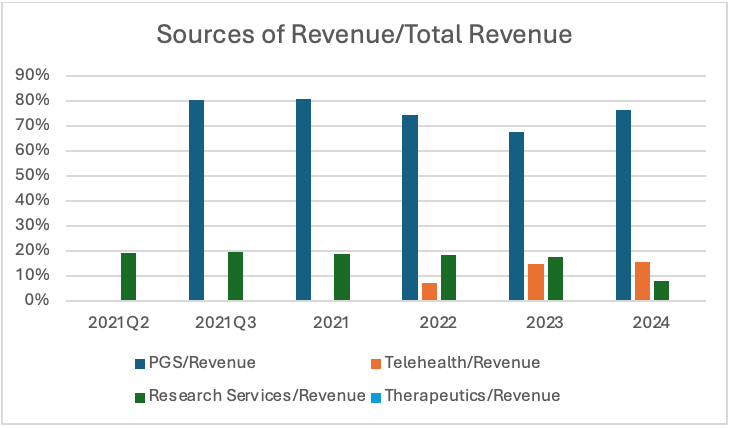

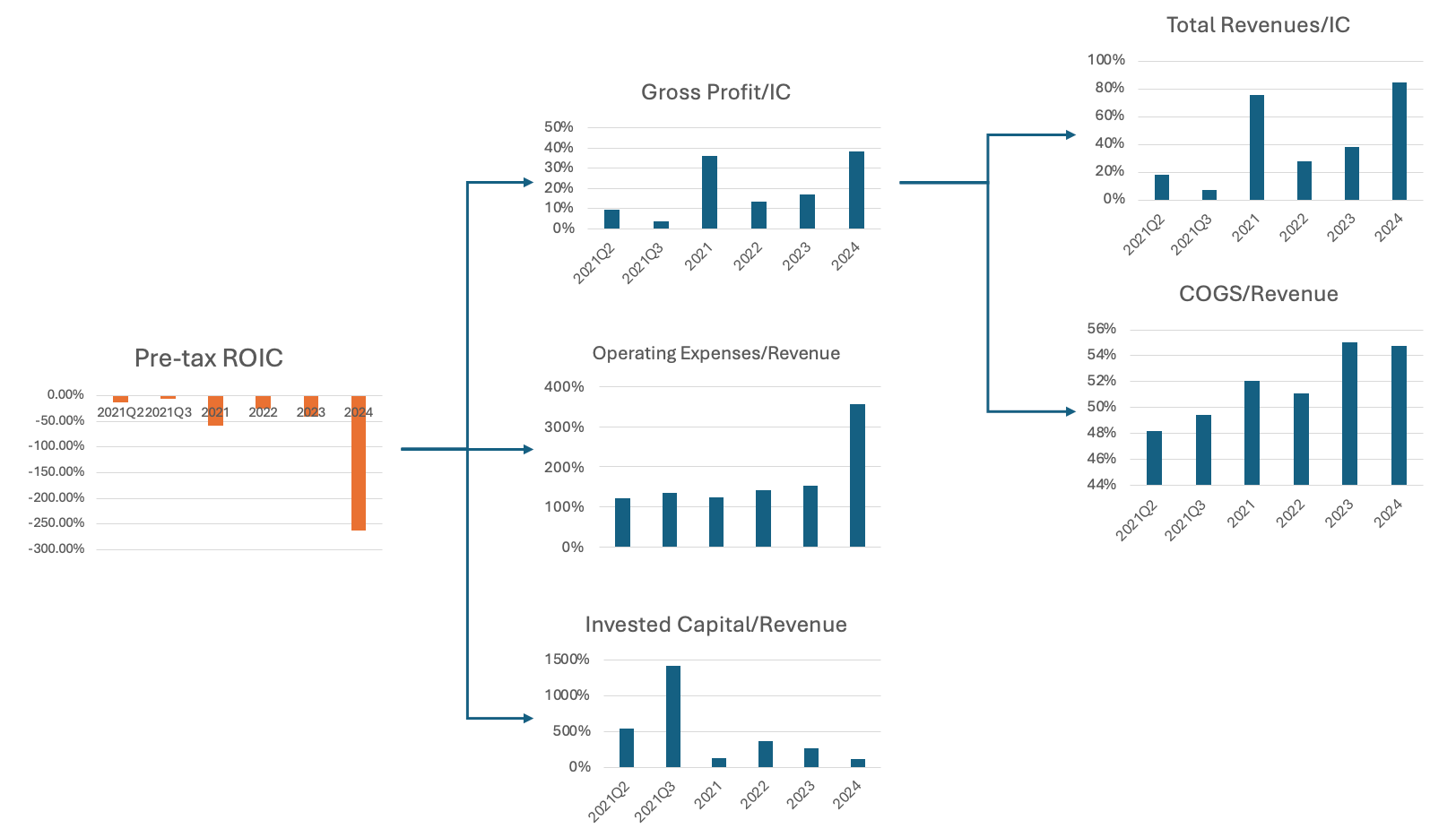

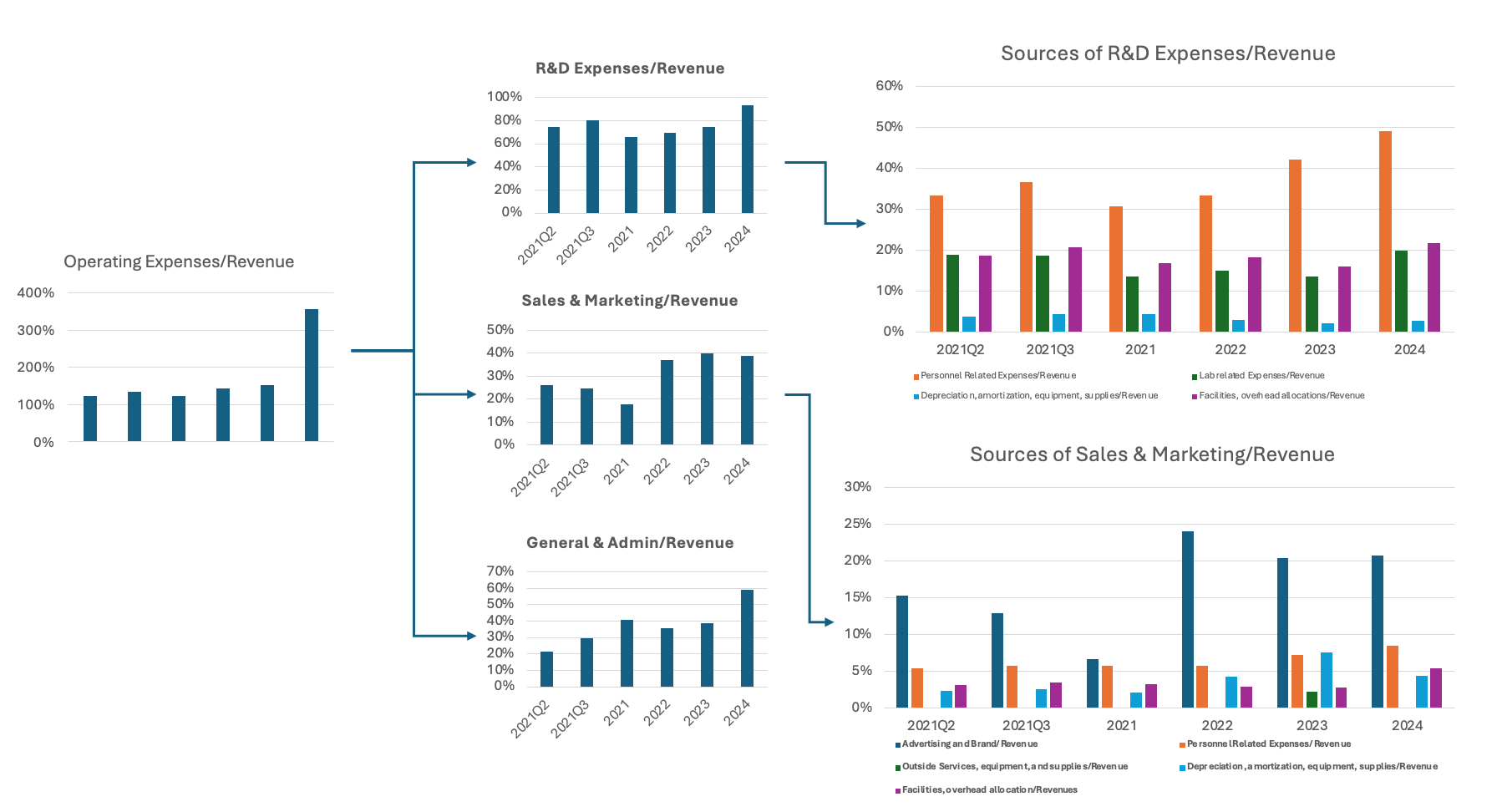

By 2024, the company had fully impaired the Lemonaid Health acquisition, writing off $351.7 million in goodwill. Simultaneously, it shuttered its therapeutics division—once considered a key differentiator—and watched 23andMe+ subscriptions decline from 640,000 to 562,000. Revenue from research services collapsed, falling from $52.5 million to $17.3 million.

Operating expenses continued to rise despite diminishing returns, and neither gross profit nor NOPAT returned to positive territory. These inefficiencies are unsustainable and point to the urgent need for strategic streamlining and financial discipline.

And perhaps most troubling: Return on Invested Capital (ROIC) fell from -41.35% in 2023 to an eye-watering -263.12% in 2024. This was not merely underperformance; it was financial freefall.

A Market Structure Not Built for Moonshots

Porter’s Five Forces offer a sobering lens on 23andMe’s operating environment. The DTC genetic testing market is saturated, highly competitive, and seasonally driven. Major competitors like AncestryDNA and MyHeritage compete aggressively on price, often slashing kit costs during shopping holidays. Customers exhibit low brand loyalty and high price sensitivity. The buyer, in this case, has near-total power.

Regulatory complexity further complicates matters. FDA clearances, while a relative advantage, also require costly ongoing compliance. Meanwhile, the company's ability to commercialize its vast genetic data is constrained by HIPAA, GDPR, CCPA, and rising public scrutiny around data privacy and bioethics.

And while 23andMe’s scientific credibility is genuine, the core consumer product remains commoditized. As other forms of digital wellness proliferate—from wearables to AI-based coaching—the company faces not just rivals, but substitutes.

23andMe’s relative strengths—its database, brand equity, and regulatory head start—remain real, but not unassailable. Its most significant moat is no longer its product, but its past.

Governance and the Illusion of Control

Strategic overreach was matched by internal disarray. In late 2024, all independent board members resigned, citing governance breakdowns and lack of transparency. CEO Anne Wojcicki’s push to take the company private was met with investor skepticism, not enthusiasm. Internally, morale declined amid layoffs and failed integrations. Even in a biotech context—where ambition often outpaces execution—this level of internal churn was notable.

The organizational structure became increasingly muddled. Research, consumer operations, and health services began to overlap without clear accountability. The dismantling of the therapeutics division suggested both capital scarcity and loss of strategic conviction.

This is a textbook example of what happens when a company tries to stretch its brand beyond what its customers, employees, and board recognize as authentic.

Strategic Identity Crisis

The root of 23andMe’s crisis lies in its identity: it is a consumer brand trying to act like a biotech firm. Its customers see it as a sentimental, curiosity-driven gift product. Its leadership sees it as a precision health platform. The market has not reconciled these two realities—and the attempt to force convergence has led to mistrust, disengagement, and operational bloat.

From a resource-based view, 23andMe’s assets remain enviable: a large and consented dataset, strong brand awareness, and a consumer-friendly product interface. But its capabilities—particularly in integrating acquisitions, sustaining subscriptions, and innovating in healthcare delivery—have fallen short.

The company's future depends on realignment: a strategic narrowing that honors the trust-based consumer experience, while insulating its more experimental ventures in R&D and telehealth under separate brands or business units.

Conclusion: A DNA Company That Needs to Do Less, Better

There’s a reason they say "know thyself"—and never has that advice been more relevant than for a company literally built on genetic self-awareness.

23andMe started out as the feel-good science gift of the decade: a $99 tube of spit that promised to tell you whether you were part Viking or just bad at digesting dairy. But somewhere between becoming a household name and a publicly traded entity, the company began reaching far beyond its consumer roots—into pharma, into telehealth, into subscription models, and eventually into strategic purgatory.

Its post-IPO saga reads like a business school case study on ambition unmoored from focus: a $6 billion valuation, a $425 million telehealth acquisition, and a -263.12% return on invested capital. Throw in the board resignations and the write-off of said acquisition, and you have a company that could use a stiff drink and a strategic reset.

To Go Private, or Not to Go Private?

Now, in a twist worthy of biotech Shakespeare, CEO Anne Wojcicki is looking to take the company private again. The rationale? Ditch the quarterly performance circus, focus on long-term planning, and innovate without market pressure breathing down the company’s neck. While the proposal was rejected, there’s logic to it—restructuring is always easier when you don’t have to explain it to every retail investor with a Robinhood account.

But let’s not romanticize it. Going private also means restricted access to capital, heightened governance risk (especially when your independent board just peaced out), and no public accountability. If 23andMe doesn’t have a clear and credible path to strategic coherence, private ownership won’t solve the problem—it’ll just make the implosion quieter.

The Real Diagnosis: Brand Identity Disorder

At its core, 23andMe has a brand problem masquerading as a business problem. Consumers still see it as a novelty—a curiosity-powered ancestry and health companion that makes for a great holiday gift. The company, meanwhile, has spent the last five years trying to convince everyone it’s actually a vertically integrated precision medicine platform.

Spoiler: it can’t be both.

Which brings us to the solution—not less ambition, but more structure.

Let’s be clear: no one’s saying 23andMe needs to scale back its vision. But it does need to stop asking one brand to carry the weight of a cocktail-party conversation starter, a clinical diagnostics platform, a drug discovery engine, and a telehealth provider. That’s not strategy—it’s brand contortion.

So, allow a thought experiment.

Imagine 23andMe adopting a clean brand architecture—one that separates consumer curiosity from clinical complexity. To make the point, let’s give this fictional structure a name: Genome & Tonic. No, it’s not real. Yes, it should be.

In this illustrative split:

23andMe returns to its roots: the emotionally resonant, data-flavored gift that tells you you’re 2% Sardinian and maybe a little predisposed to hating cilantro. No health claims. No clinical overreach. Just accessible science and light storytelling.

Lemonaid Health gets the clinical spotlight it wants as a separate telehealth brand. Think: “Your prescription, without the waiting room.” It can pursue scale in digital care without dragging the consumer brand into HIPAA headaches.

Full Stack Bio (yes, another invented name) becomes the quiet, serious engine behind pharma partnerships and R&D. No branding gymnastics, no lifestyle messaging. Just pipelines, platforms, and NDAs - “Biology. End-to-end.”

At the top, Genome & Tonic plays parent: an umbrella brand that gives each business room to grow without making them all share a toothbrush. Tagline? “Refreshing insights, sequenced not stirred.” (Because even imaginary holding companies deserve a little flair.)

Do Less. Do It Better.

Here’s the real point: 23andMe doesn’t need another pivot. It needs a plan.

It already has the raw materials—a massive dataset, early regulatory wins, and a consumer base that still wants to like the brand. What it lacks is coherence. Stop asking a single brand to do four incompatible jobs. Stop confusing consumers with clinical ambitions they didn’t sign up for. Stop playing biotech on hard mode.

The future isn’t about being less ambitious—it’s about being architecturally sane. And if that comes with a martini and some better segmentation? Even better.

Great article, Swetha! “Genome Tonic — Refreshing insights, sequenced not stirred” is simply a masterpiece 🙇🏻♀️